Brazil is the third largest Producer of Chicken Meat in the World and ranks first in World Exports.

Brazil is the 3rd largest producer of broilers in the world and the 1st place in exports.

Brazil is the third largest producer of chicken meat in the world, behind the United States (USA) and China. In 2009 it surpassed the USA, reaching the 1st place in exports. It also occupies a good position in egg production, 7th place. Poultry production generates around 2 million direct and indirect jobs throughout Brazil, contributing to a significant increase in the economy. The south and southeast regions are the largest producers, but there is a growing production in the center-west region due to the production of corn and soybeans. The states that produce the most chicken are the states of Paraná (27%), Santa Catarina (26%) and Rio Grande do Sul (23%). The low cost with investment in facilities and high production of grains, favors the production of chickens in Brazil.

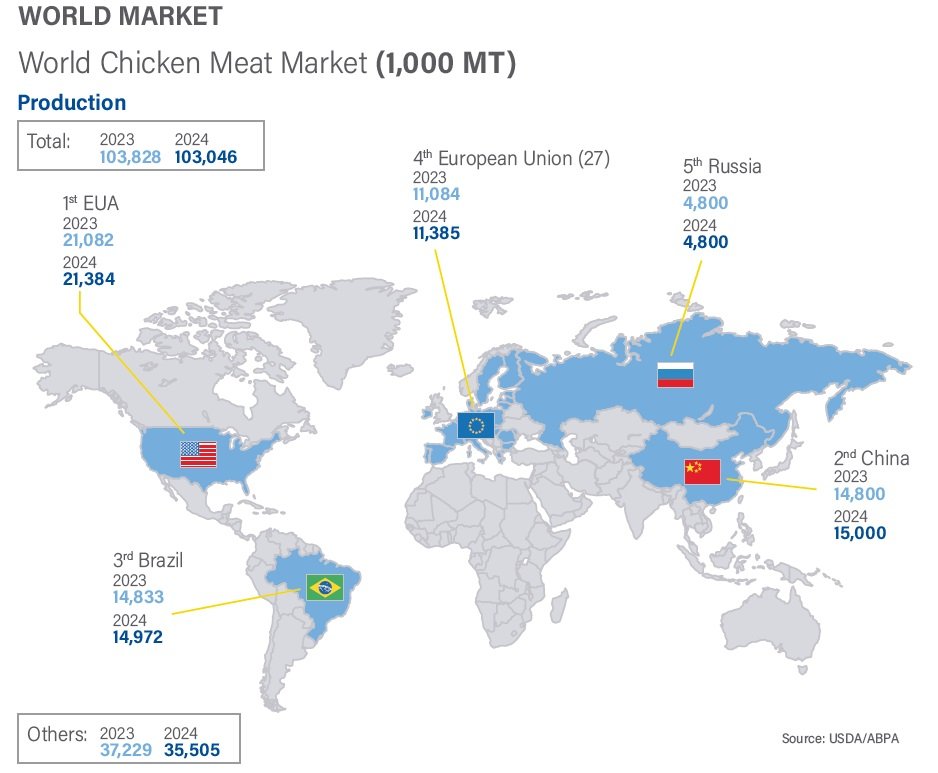

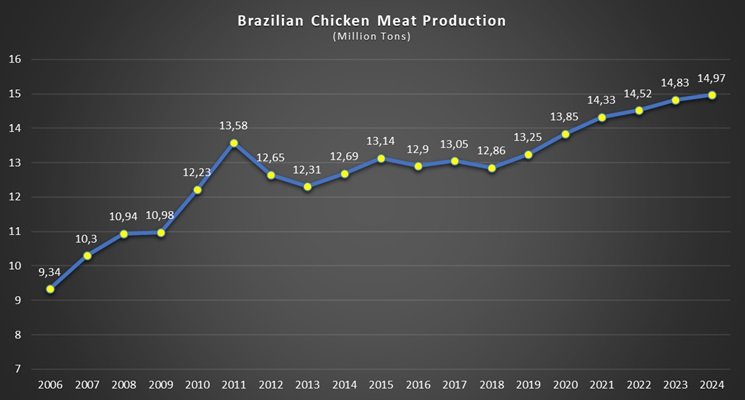

In 2021, China surpassed Brazil in chicken meat production by 200,000 tons, placing China in second place in the world rankings and Brazil in third. In 2023, Brazil surpassed China in production by 33,000 tons, thus regaining second place, but in 2024, China increased its production to 15 million tons, again surpassing Brazil by 28,000 tons. Thus, in 2024, Brazil remains the third-largest chicken meat producer in the world with 14.972 billion tons.

Chicken Meat Production should have Record Yield in 2025/26 in Brazil

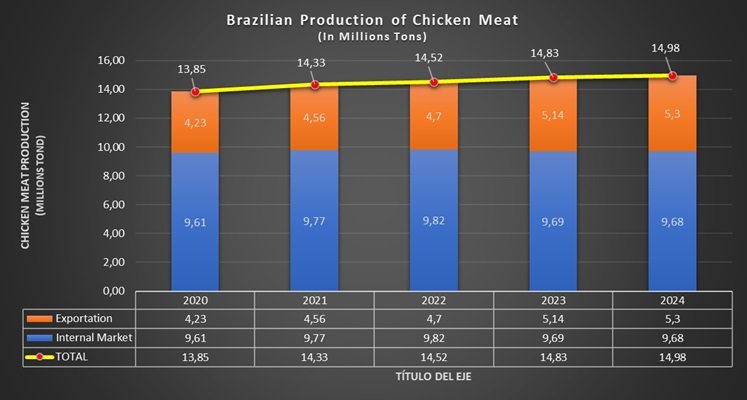

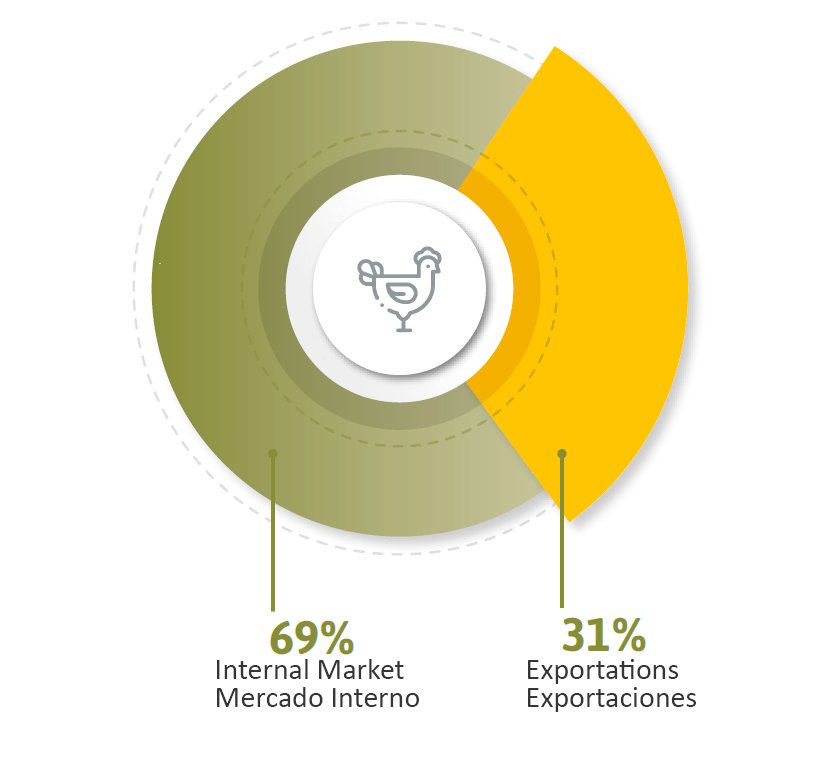

Chicken meat, Brazil’s main protein on the international stage, was also discussed in detail. Production is expected to reach 15.4 million tons in 2025, and a further increase is estimated for 2026, reaching 15.7 million tons. Brazilian exports are expected to decline slightly in 2025. Shipments are forecast to total 5.2 million tons, compared to 5.29 million tons in 2024. This drop of up to 2% reflects the temporary impact of avian flu and the restrictions imposed by some markets. However, the sector is already negotiating the reopening of these destinations and expects to reach 5.5 million tons exported in 2026, an increase of 5.8%. In the Brazilian domestic market, availability is also growing. Per capita consumption is expected to reach 2,025 kilograms in 47.8 years, up from 45.5 kilograms in 2024. For the ABPA, this guarantees stable production and strengthens exporters’ confidence, keeping Brazil at the top of the list of global suppliers.

Evolution of Brazilian Chicken Meat Production

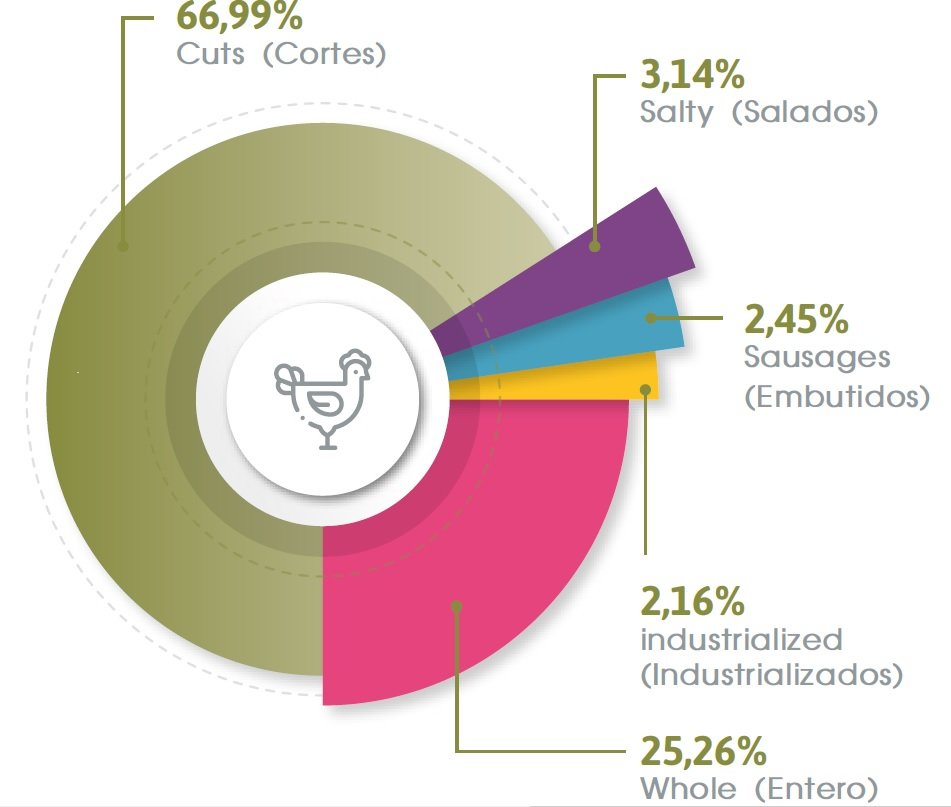

Brazilian chicken meat by destination

BRAZILIAN EXPORTS OF CHICKEN MEAT

According to data from the Secretariat of Trade and International Relations of the Ministry of Agriculture and Livestock (SCRI/MAPA), from January to July 2025 alone, exports of chicken meat and offal exceeded US$5.47 billion, totaling more than 2.9 million tons. The main destinations for Brazilian chicken meat are: Saudi Arabia, China, the United Arab Emirates, Japan, Mexico, and the Philippines. For chicken offal, the destinations are: China, Hong Kong, Ghana, and Saudi Arabia. According to the National Supply Company (CONAB), chicken meat production is estimated to reach a new record in 2025, projected at 15.48 million tons, a 1.5% increase compared to 2024.

Brazil, the world leader in exports of the product, will be responsible for more than a third of the estimated increase, as “is well positioned to profit from growing demand from the European Union and the UK.” The forecast is something around 4.180 million tons of in natura product.

For the USDA, Brazil is also able to meet the growing imports from East Asia and the Middle East. But he points out that the increase in demand from Asia, especially from Japan and China, will also support the expansion of exports from Thailand. The US agriculture body ends its analysis by noting that, despite the increase in domestic production, chicken meat imports from China will remain firm. The expected increase will be limited, not reaching 3%. Note that, in all its projections, the USDA continues to disregard exports and imports of chicken feet/paws. Therefore, the effective values will be higher than those indicated, especially with regard to Brazil and China.

It is the most popular species, desired and marketed worldwide. It has a milder flavor than the other species. It is a large salmon with an elongated body, with an exclusive silver color, with black dots on its body. Versatile and fresh for all types of cuts and preparations. Its colorful color is very typical of this species.

Chile is one of the world's largest producers of this species, which is harvested between the months of September and February. It has been the traditional product for the Japanese market in its frozen presentation. In recent years, Trim C Filet has been produced, which has diversified to other markets. It is characterized by its red color. Its main destinations are Japan, the People's Republic of China, Thailand and South Korea.

Chile is the world's leading producer of seawater farmed trout. It is characterized by the intense red color in its meat and a spectacular texture and flavor. It is highly desired by the sushi market. The main markets where it arrives are Japan, Thailand, the United States, Russia and China.

Previous

Next

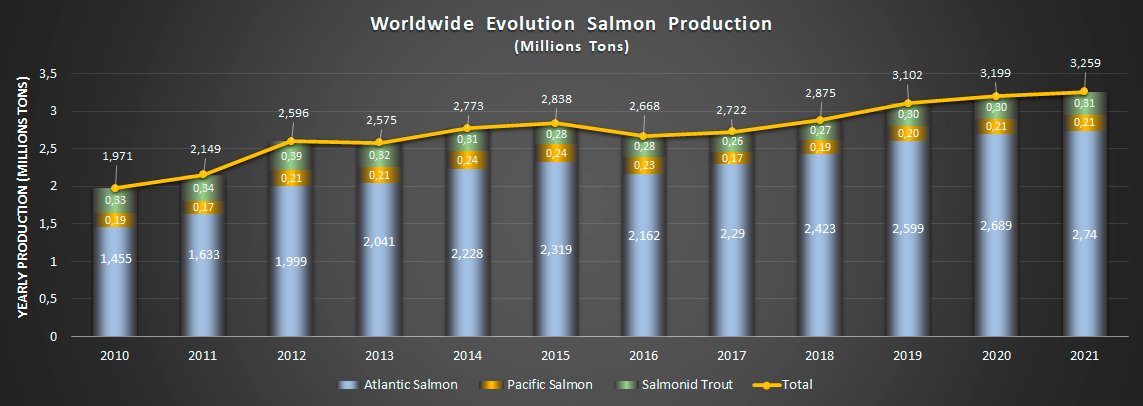

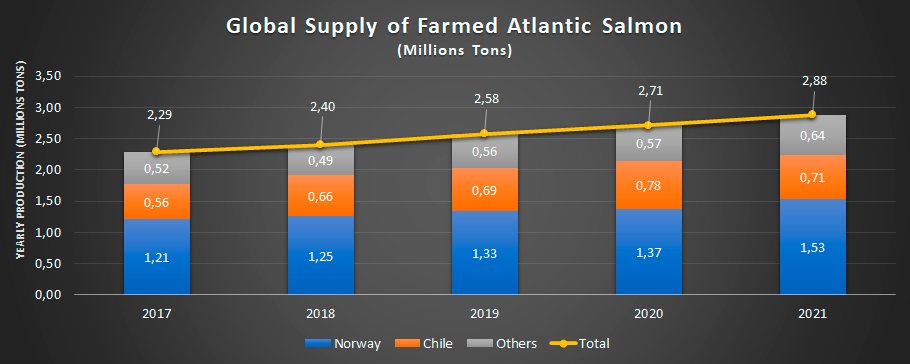

Global supply of Atlantic salmon maintained strong y-o-y volume growth in 2021

The global harvest of farmed Atlantic salmon increased by an estimated 168,000 tonnes (+6.2%) y-o-y during calendar year (CY) 2021 to 2.88 million tonnes. The growth was driven by robust Norwegian supply, where technological innovation, alongside plentiful feed availability from Jul-Oct ‘21, facilitated larger individual fish. Unseasonably warm seawater temperatures during the second-half of the CY 2022 (H2 2022) also contributed to atypically fast smolt growth. These factors resulted in estimated Norwegian salmon supply increasing by approximately 151,848 tonnes (+11.1%) y-o-y in 2021 to 1.52 million tonnes

Mintec anticipates that Norwegian supply may tighten during the first-half of CY 2022 (H1 2022) versus H1 2021. This is based on a comparatively smaller biomass of 332,400 tonnes present on 1st Jan ‘22, compared to 370,300 tonnes for 1st Jan ‘21.

The lower biomass accounts for 10,300 fewer live fish y-o-y on 1st Jan ‘21, despite slightly higher weight per fish (4.1kg in Jan ’22 vs 4.0kg in Jan ’21)

The strong y-o-y growth recorded in Norwegian salmon production during the 2021 CY helped offset lower Chilean supply, which contracted by 72,000 tonnes (-9.3%) during the same period to 706,000 tonnes. This decline came as a reaction to weak demand and profitability in 2020, which prompted Chilean farmers to reduce restocking activities. High fish mortality rates associated with sea lice infestations and algae blooms further stunted Chilean farm yields in 2021. However, Chilean production is expected to accelerate during H1 2022, largely in response to the higher average prices and profitability gains recorded in CY 2021. The likelihood of firm demand from the Americas and Europe provides further impetus for the Chilean supply outlook

Worldwide Salmon Production (Millions tons)

Total Production in 2021: 3,259 millions tons

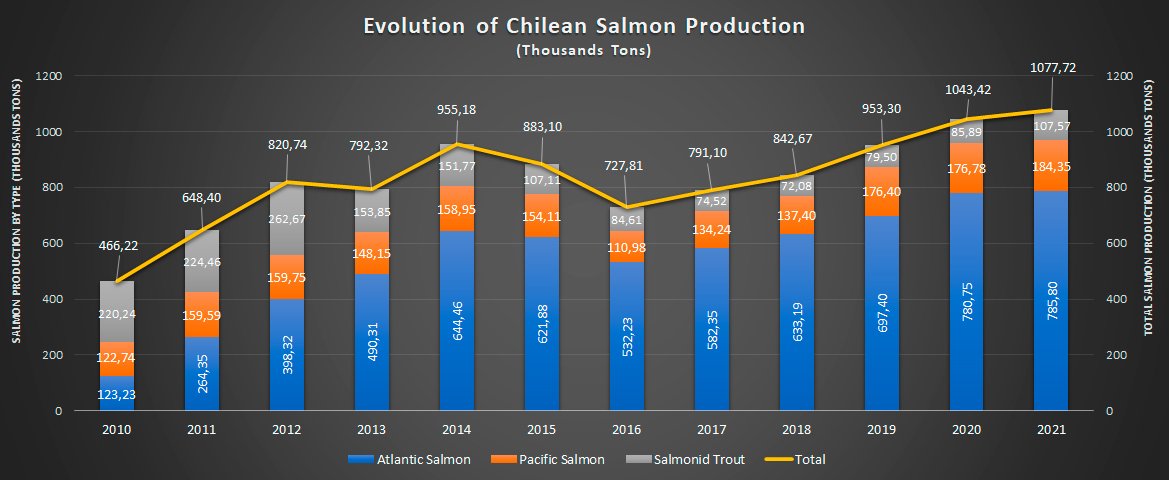

Chilean Salmon Production

Chile is the second producer of salmon globally, behind Norway. It concentrates around 27% of global production. Exports of this product ranked second after copper in 2021.

In 2020, the Chilean salmon industry exceeded the barrier of one million tons of harvest for the first time and for the second consecutive year it recorded the highest production in its history.

This was stated by the National Fisheries and Aquaculture Service (Sernapesca) in its 2020 Fisheries and Aquaculture Statistical Yearbook published by the agency last Friday, May 28.

The document details that in the last year the industry harvested 1,079,595 tons, the highest volume in its 40-year history. The figure represents an increase of 9.1% compared to 2019, when the sector had reached a production of 989,546 tons.

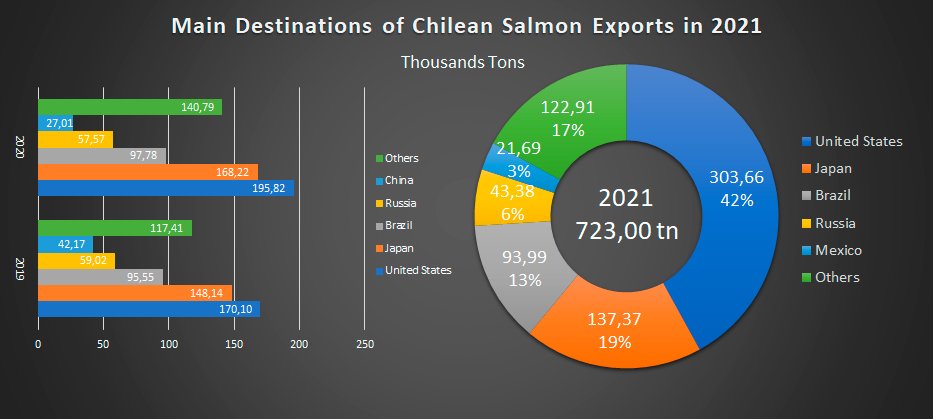

Chilean Salmon Exportations

Chilean salmon exports experienced a significant jump in 2021, returning to pre-pandemic levels. In addition, this sector ranked second in export value last year, ranking behind copper. Salmon exports reached US$ 5,180 million, which represents a jump of 18.2% compared to the previous year, according to the annual report on salmon exports, prepared by the Chilean Salmon Council. In 2020, meanwhile, while the coronavirus gave no respite and hit the world hard, salmon exports fell by 14.9% compared to the previous year.

“There was a progressive recovery in salmon exports as 2021 progressed. Thus, while shipments fell 2.6% annually in the first quarter, increases of 11.6% were recorded in the second and third quarters. and 33.4% respectively when comparing them with the same quarters of the previous year. Finally, salmon and trout exports totaled US$1,549 million in the fourth quarter of 2021, 37.5% higher than the same quarter of the previous year,” the report indicated.

The main destination market for Chilean salmon in 2021 was the United States, followed by Japan, Brazil, Russia and Mexico. These five countries accounted for more than 85% of local exports of this product. The recovery in demand was led by the US and Brazil, with an annual increase of 33.7% and 63.5% respectively. Shipments to China and Russia, meanwhile, were down compared to 2020.

The outlook for the current year in the industry is positive, as long as the pandemic remains under control, and the dynamism in the growth of new distribution channels continues.

“We hope that there will be no greater restrictions due to covid after the Ómicron outbreak and that the opening of hotels and restaurants can continue, which, added to the growth of new distribution channels such as online and retail sales, allow us to maintain good projections for salmon farming. for this year that has just begun,” said Joanna Davidovich, executive president of the Salmon Council.

“The growth of salmon and trout exports has been greater in the last 10 years than that of total exports and that of the rest of the “non-copper” goods, with which they have been gaining relevance within total Chilean exports. , going from representing 6.9% of “non-copper” exports in 2010 to 12.5% in 2021″

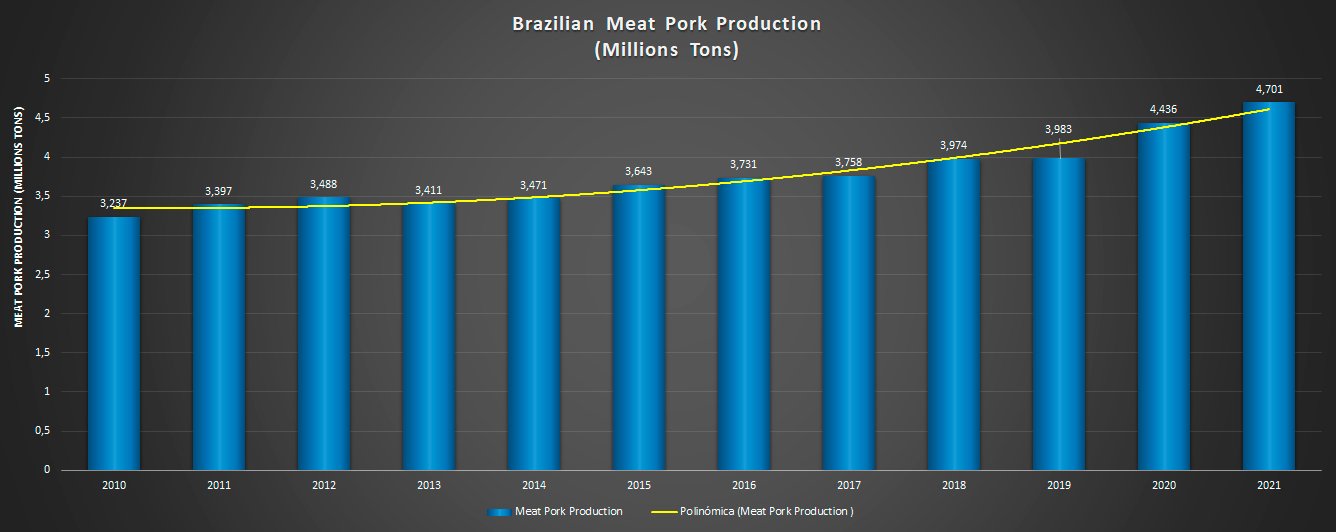

Data released by the Brazilian Animal Protein Association through its annual report indicates that Brazilian pork production showed a new increase over the past year. The volume produced reached 4.701 million tons, representing an annual growth of 6%, while in the decade the increase reached 38.4%.

Although producing enough volume to supply the domestic market and continue to advance in the international market, swine farmers suffered serious losses during the year. The cost of feed had a strong impact on the result as they were not able to market their product in the same proportion.

Brazilian Pork production first quarter of 2022

At the end of the first quarter of 2022, the slaughter of pigs increased by 7.2% compared to the same period of the previous year, from 12,721,000 to 13,637,038 head (cb). Likewise, pork production increased by 6.7% in the same period, reaching 1,244 thousand tons (mt).

Regarding exports, they reached 232 mt in the first quarter of 2022, a value that represents a drop of 6.7% compared to the same period of the previous year (249 mt). The main exported products corresponded to frozen meats with a share of 89%, followed by boneless offals and hams, which represented 6.5% and 2.3% of the general total, respectively.

Annual estimates of swine production in Brazil

Based on data from the Brazilian Institute of Geography and Statistics (IBGE), maintaining the averages of the first quarter, until the end of 2022, the slaughter of pigs will grow 2.99% compared to 2021, reaching 54,548,000 cb. Likewise, a production of 4,976 mt is projected, which would represent a growth of 1.75% in relation to the previous year and a per capita consumption of 19.2 Kg/inhabitant. However, it is very likely that in the second half of the year there will be a reduction in production, as a result of the reduction in sows that took place in recent months, due to the crisis in the sector.

On the other hand, according to the latest estimate report for swine and poultry, published by the USDA Foreign Agricultural Service on April 6, annual exports would be around 1,330 mt, i.e. an increase of 0.7% in compared to 2021, while the volume of imports would remain at 3 mt.

Brazil is one of the most important beef producers in the world, the result of decades of investment in technology that not only increased productivity but also the quality of the Brazilian product, making it competitive and reaching the market of more than 150 countries.

USDA data points to a 7.7% drop last year and a 4.6% increase for 2022

In its report released last January on the world trade in livestock and poultry, the USDA pointed to a strong retraction in Brazilian beef production last year and a new recovery in the course of 2022.

According to the USDA, Brazil produced about 9.325 million tons of beef in 2021, equivalent to the worst volume of the last five years and meaning an annual retraction of 7.7%.

The previous forecast for last year reached 9.500 million tons. However, with the reports pointed out by Brazil from September of the detection of atypical bovine spongiform encephalopathy (BSE), China temporarily restricted beef imports, bringing down Brazilian slaughter in the fourth quarter. This impacted by almost 2% less the volume that already had a strong retraction.

However, with the issue resolved, strong demand from China should help stimulate beef production in Brazil in 2022. Estimated production for the current year is 9.750 million tons, an annual increase of 4.6%. Even so, if indeed achieved, it would mean the second lowest volume in six years.

Brazilian Beef Exports

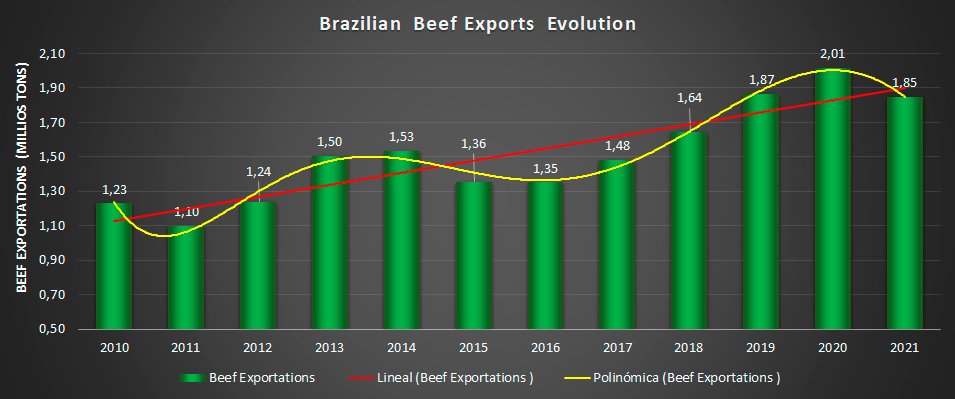

Total beef exports in 2021 (including fresh and processed products) showed a 7% drop in volume and a 9% growth in revenue compared to the 2020 movement, according to the Brazilian Meatpacking Association (Abrafrigo). The entity compiled the data from the Ministry of Economy’s Foreign Trade Secretariat.

According to Abrafrigo, the country handled 1,867,594 tons in 2021 compared to 2,016,223 tons in 2020, a record year for exports. Thanks to the product’s price hike in international markets, however, revenue rose from $8.485 billion in 2020 to $9.236 billion in 2021.

The total movement of beef in the last month of the year reached 151,593 tonnes, against 168,155 tonnes in 2020, down 10%, according to the entity.

The revenue obtained was US$ 726.6 million, against US$ 741.2 million in 2020, a reduction of 2%.

Brazilian Beef Exports

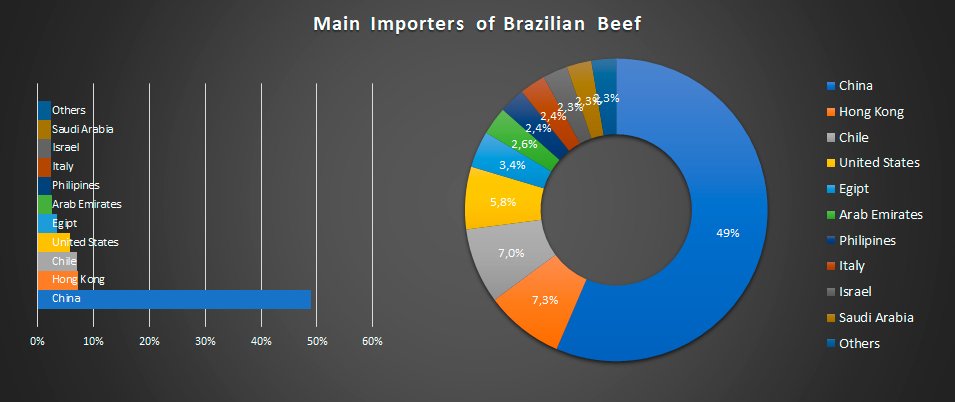

Although it reduced its imports from 1,182,673 tonnes in 2020 to 950,057 tonnes in 2021, China remains the biggest buyer of Brazilian beef, through the movement carried out by the city-state of Hong Kong and through purchases made by the mainland.

Abrafrigo reports that, last year, the United States became the second largest importer of the product, from acquisitions of 59,545 tons in 2020 to 148,177 tons in 2021, with an increase of 148.9% in handling. Chile remained in third position, going from 90,403 tonnes imported in 2020 to 110,626 tonnes in 2021 (+22.4%). Even reducing its purchases by 42.5%, from 127,953 tonnes to 73,612 tonnes, Egypt ranked fourth. The United Arab Emirates increased its imports by 21.7%, from 40,861 tonnes in 2020 to 49,711 tonnes in 2021, ranking fifth. In sixth place, the Philippines went from 39,673 tonnes in 2020 to 46,349 tonnes in 2021 (+16.8%), while Saudi Arabia was seventh with a 0.5% drop in handling, which went from 41,067 tonnes in 2020. to 40,870 tons in 2021.

Argentine Beef

Cattle slaughter during the fourth quarter of 2021 stood at levels slightly above 3.31 million head, a similar amount (0.0%) to the values corresponding to the third quarter of 2021, when also slaughtered approximately 3.31 million bovines. Compared to the fourth quarter of 2020, when about 3.64 million heads had been slaughtered, cattle slaughter showed significant falls (-9.2%). Of the 334 thousand heads less slaughtered in relation to the fourth quarter of 2020: 192.3 thousand were steers and young bulls and 6.4 thousand bulls, to which must be added the decrease of 43 thousand cows and more than 92 thousand heifers in the task.

During the year 2021, bovine slaughter has been close to 13 million head, (-7.3%) below the values corresponding to the period January – December 2020, in which about 14 million head had been slaughtered. cattle. The significant decline observed in bovine slaughter, which is over a million heads, is explained by a drop in the slaughter of steers and heifers, of about 354 thousand heads, and of heifers, by about 400 thousand, which was accompanied by a lower slaughter of cows, less by about 257.5 thousand heads than the previous year, and also due to fewer bulls, about 14 thousand.

Throughout the fourth quarter of 2021, approximately 762.4 thousand tons of bone-in beef were produced; a slightly lower volume, (-1.5%), than that obtained during the third quarter of 2021, and, in addition, it was (-7.9%) lower than the volume of production processed during the fourth quarter of 2020, which had been close to 828 thousand tons. Comparing the volume of beef production in the fourth quarter of 2021 with that obtained throughout the same quarter of 2020, a year-on-year contraction of (-7.9%) is observed; in the same period of time, the fall registered in the number of slaughtered animals was (-9.2%). The improvement in the average weight of carcasses, which went from 227.2 to 230.4 kilograms, explains why production reacted 1.3 percentage points below the slaughter cut.

Beef production in the fourth quarter of 2021 showed slight falls in terms of its aggregate volume of production in relation to the third quarter of 2021, going from 774 thousand tons of bone-in beef equivalent to 762 thousand tons.

To round off this drop, 15.4 thousand tons less of steer and young bull meat were produced (-3.4%), 10.4 thousand tons less of beef (-8.0%); and 0.5 thousand tons less of bull meat (-3.2%); and in the opposite direction, 14.7 thousand tons more of heifer meat were produced, (+8.2%); leading to a quarterly drop in production of 11.6 thousand tons of beef, (-1.5%), comparing the fourth quarter of 2021 with the third quarter of the year.

When comparing the fourth quarter of 2021 with the same period in 2020, approximately 40.2 thousand tons less of steer meat and steers (-8.5%) were produced, 16.3 thousand tons less of heifer meat , (-7.7%); 7.1 thousand tons less of beef from cows (-5.6%), and 1.7 thousand tons less from beef from bulls, (-9.5%), resulting in a year-on-year drop in production close to 65, 2 thousand tons, (-7.9%), which went from about 828 thousand tons in the fourth quarter of 2020 to approximately 762 thousand tons in the fourth quarter of 2021.

Argentine Exports of Bovine Meat

Argentine exports of beef accumulated over the last year, from March 2021 to February 2022, were located in volumes close to 708 thousand tons of bovine beef equivalent and 84 thousand tons of bovine bones; for a value close to 2,884 million dollars. In February 2022, foreign sales of bovine meat and bones were at significantly higher levels (+21.7%) than last January; and, they were slightly higher, (+2.5%), than those of February 2021, considering the volumes shipped in product weight tons (offals and viscera are not included). In summary, shipments of chilled, frozen cuts, and processed meat corresponding to the month of February 2022 totaled about 40,001 tons of bovine meat product weight and approximately 6.9 thousand tons of bovine bones, for a value of approximately 266, 6 million dollars. The average FOB price per ton for the period in question was approximately US$8,900 for chilled boneless cuts; and over $5,740 for boneless frozen cuts. These prices have been significantly higher, (+33.4%), than those registered during the second month of 2021 for chilled cuts; and they were (+39.7%) higher than those of February 2021 in the case of frozen cuts. The average price of February 2022 increases slightly compared to January, (+1.8%), and increases significantly compared to February 2021, (+37.8%).

Previous

Next

China absorbs more than 50% of Argentine beef exports

The People’s Republic of China was the main destination, in volume, for Argentine beef during the first two months of 2022 with approximately 63.0 thousand tons, followed by Israel, 6.43 thousand tons, and then by Chile, 3, 93 thousand tons. In terms of the value of foreign currency received, the main market during the period was China, which represents 63.5% of the total exported value of chilled, frozen and processed beef in the period, followed by Israel (9. 4%), and Germany (6.9%).

If shipments are compared in the first two months of 2022 with those corresponding to the period January to February 2021, they showed a varied behavior in relation to the levels of activity that had been registered a year ago: United States, the Netherlands and Germany show significant growth.

China, Israel and Italy exhibit moderate negative variations; while Chile, Brazil and Russia show falls of great magnitude in the volumes of Argentine meat demanded. The dependence on the Chinese market for Argentine beef exports has become decisive, and in the last month of February 2022, there were 34.5 thousand tons, which represented approximately 73.6% of shipments. Israel, with 2.6 thousand tons, became the second most relevant destination, in terms of volumes, in the month of February 2022.

Argentine beef exports fell by about 9.1 thousand tons when comparing the first two months of the last two years. Of this reduced volume, about 7.3 thousand tons correspond to lower shipments to China; and another 1.6 thousand tons correspond to Brazil and around 1.3 thousand to Chile, while the rest of the destinations as a whole accumulate an expansion close to one thousand tons.

{kind=link}

{kind=link}

{kind=link}

{kind=link}